Consumer Sentiment Jumps to New Heights

The University of Michigan released their monthly Survey of Consumers last week and the headline? Consumers continue to feel better about their personal finances and the overall economy.

The sentiment survey number moved up to 79.6 for February. It was 79 in January and 66.9 a year ago. That’s a 19% upswing over the past 12 months, and the highest confidence number in 31 months.

The conductors of the survey commented, “Consumers continued to express confidence that the slowdown in inflation and strength in labor markets would continue.”

Confidence Remains Below Pre-Pandemic Levels

It is important to point out that confidence is still below pre-pandemic levels and 6% lower than the historical average of the survey, which dates back to 1978.

Now, it can be easy to dismiss consumer thought about the economy since it is based mostly on feeling, and not data. But, how consumers feel about their personal finances is a big deal.

Consumer Spending Accounts for 70% of U.S. Economy

If people feel good about their finances, they will likely not delay planned purchases, and about 70% of the U.S. economy relies on consumer spending.

The latest survey flies against headwinds of doom and gloom, and a near-term recession.

Ryan Dietrick, Chief Market Strategist for The Carson Group, and one of the only experts who has been shouting No Recession over the past couple of years, makes the claim that consumers and households could be in the best shape in decades.

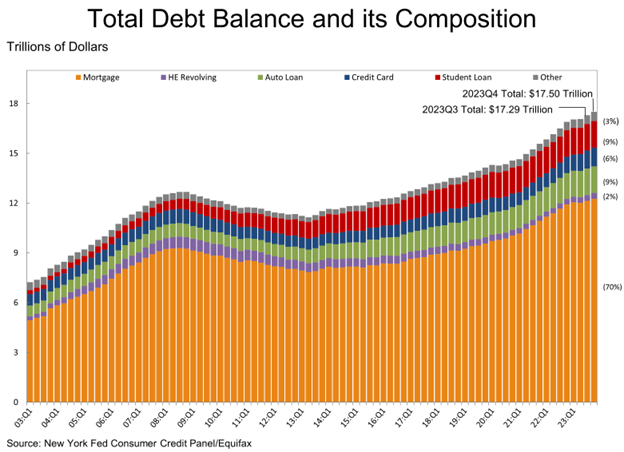

How could this be? Well, he notes that while overall debt for U.S households is up to a record $17.5 trillion, disposable household income increased to $1.33 trillion. That’s up 6.9% over the previous 12 months.

Check out his chart that breaks down the types of debt we carry.

It tracks debt over the past 20 years. We are seeing that overall number grow. Mortgage debt is far and away where most of our debt is. $583 billion, or 70% of our household debt. Auto loans and student loan debt are 9% each, and credit cards make up 6% of our overall debt.

Analyzing Growth in Disposable Income

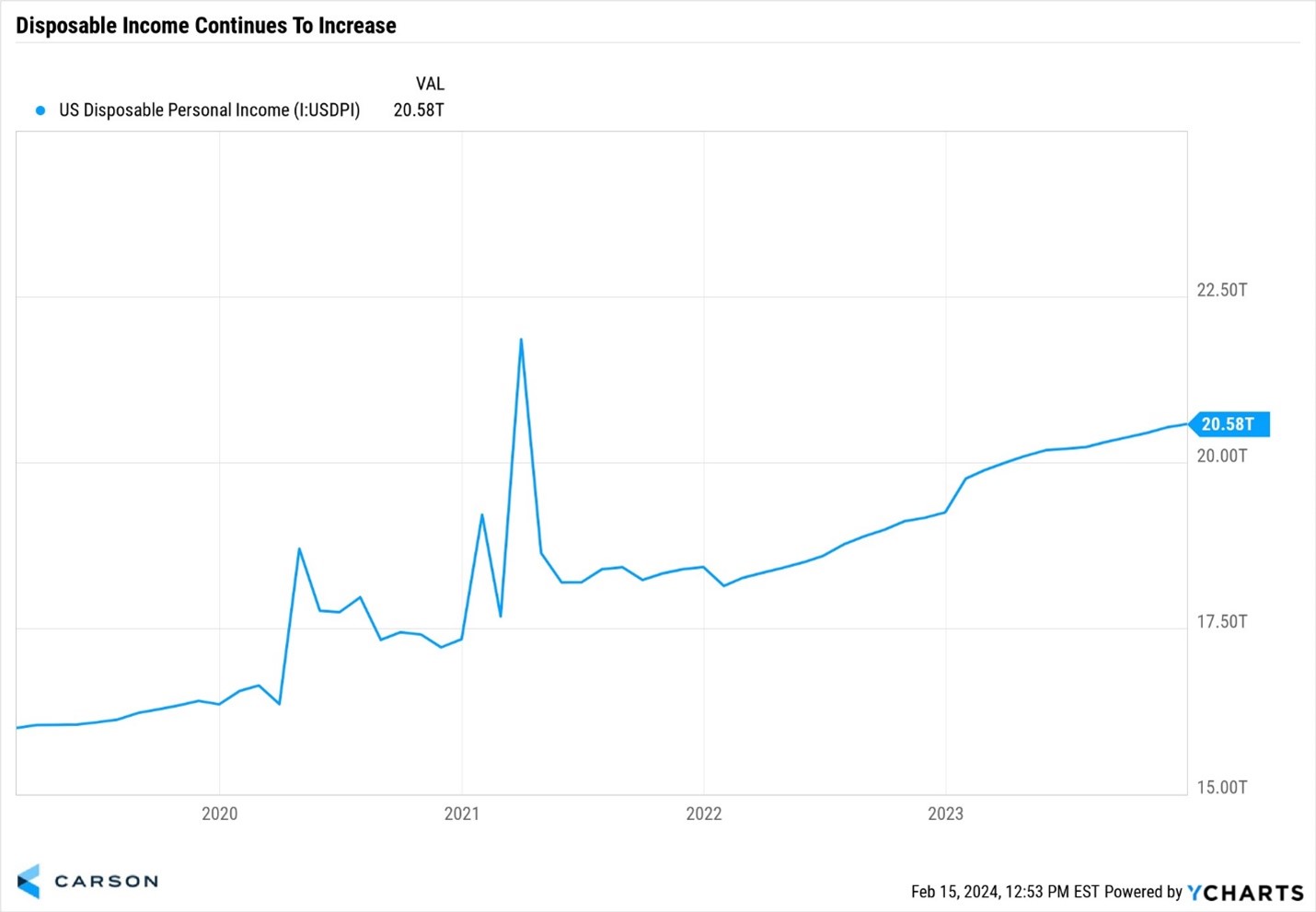

But, look at the next chart showing disposable income.

You can see the spike in 2021, caused by the extra money that the government injected into the economy. But, after the drop off in the middle of 2021, disposable income is rising steadily. Higher now, that before the pandemic.

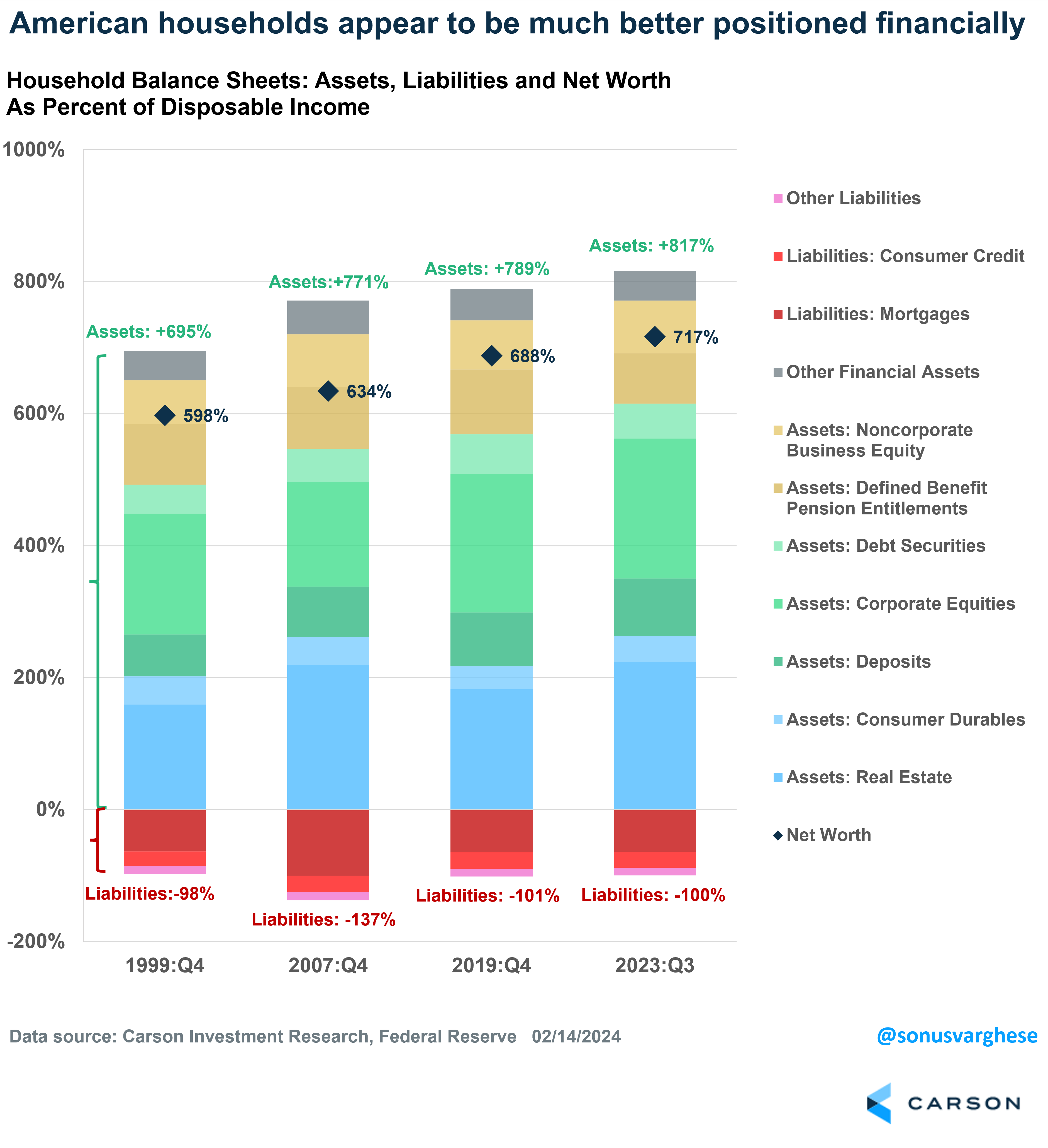

One more chart for you. This one shows household balance sheets.

You can see that as of the 3rd quarter of 2023, that debt, as a percentage of disposable income, is about where it was in 1999, and lower than 2007.

Household Debt-to-Income Ratio Reaches 20-Year Low

Bottom line: the inflation rate is now much lower than the growth in household disposable income. That could mean that the consumer has weathered the price increases, and is reaching some solid footing, which could tell us the economy is stronger than a lot of people think.

Past performance isn’t indicative of future results. All information contained in this blog is for general information only and shouldn’t be considered investment advice.

{kind=link}

{kind=link}

{kind=link}